Every Income Property,

Measured to the Inch.

We specialize exclusively in 2–4 unit residential income properties. No single-family detours, no commercial overreach — just the asset class where our methodology is sharpest.

Duplex

Side-by-side and stacked configurations. Full interior access with rental schedule analysis.

Triplex

Mixed-use capable. Income approach weighted with gross rent multiplier and cap rate.

Fourplex

Maximum conforming unit count. Full DCR analysis included for commercial lender submissions.

Standard Turnaround

Completed Annually

FNMA Forms

Geographic Coverage

Three Lenses.

One Defensible Opinion.

USPAP-compliant analysis means every conclusion is traceable to market evidence. We document the reasoning so the underwriter doesn't have to guess.

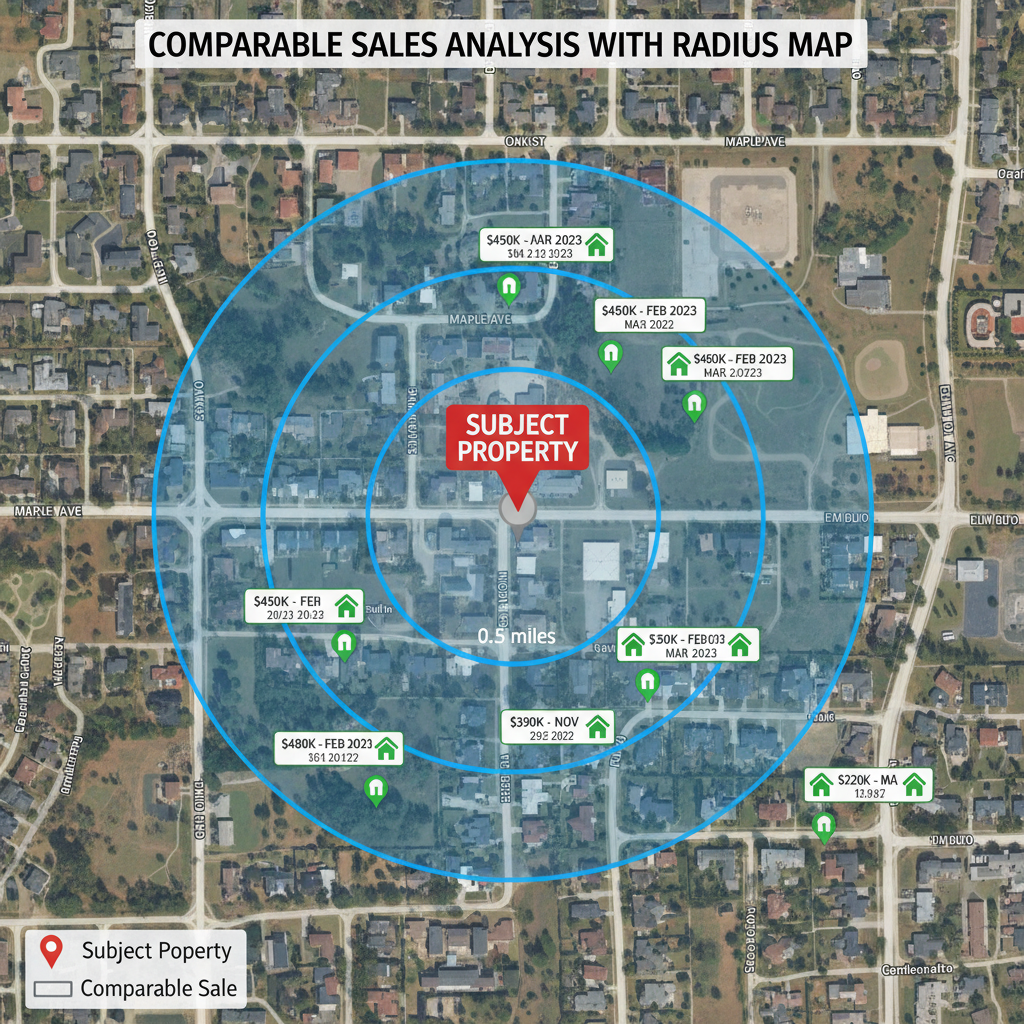

Sales Comparison Approach

We identify three to five closed comparables within a defined radius, applying defensible adjustments for GLA, unit configuration, condition, and concessions. Every adjustment line is bracketed and justified against paired-sale data — not appraiser opinion.

Income Approach

Gross Rent Multiplier and direct capitalization are applied to the subject's actual and market rent schedule. We derive GRM from comparable rentals and extract cap rates from verified investor transactions — not published surveys.

Cost Approach

Marshall & Swift cost manuals anchor our replacement cost estimates. Depreciation is measured physically, functionally, and externally — documented with photographs. Land value is extracted from improved sales using abstraction, not assessment ratios.

Every Adjustment Line

Justified in Writing.

The grid below is drawn from an actual appraisal. Every adjustment is bracketed by paired-sale evidence. Underwriters receive a report where nothing requires follow-up.

Free Download

What Lenders Look For in a Multi-Family Appraisal

12-page PDF covering underwriter checklist items, common report deficiencies, and how to read an adjustment grid.

Download PDF| Adjustment Item | Subject | Comparable 1 | Comparable 2 | Comparable 3 |

|---|---|---|---|---|

| Sale Price | — | $385,000 | $412,000 | $368,000 |

| Sale Date | Current | 3 mo ago +0 | 5 mo ago +$2,100 | 7 mo ago +$4,200 |

| Gross Liv. Area | 2,840 sf | 2,760 sf +$3,200 | 2,920 sf -$3,200 | 2,680 sf +$6,400 |

| Unit Count | 2 | 2 0 | 2 0 | 2 0 |

| Condition | Good | Good 0 | Avg+ +$8,000 | Good 0 |

| Garage | 2-car | 1-car +$5,500 | 2-car 0 | None +$11,000 |

| Net Adjustment | — | +$8,700 | +$6,900 | +$21,600 |

| Adj. Sale Price | — | $393,700 | $418,900 | $389,600 |

The Report Held Up.

Every Time.

The adjustment grid came back with every line bracketed against a verified paired sale. Our underwriter had zero conditions on the appraisal — that's the first time that's happened on a multi-family submission this year.

Marcus Delgado

VP of Commercial Lending

Meridian Community Bank

We had four siblings and three different attorneys who all wanted a different number. The report held up in mediation because every conclusion traced back to the market. Nobody could argue with the comps — they were all county-verified.

Catherine Okafor

Estate & Probate Attorney

Okafor & Reyes LLP

I've ordered 1025s from three different firms over the past two years. Appraise is the only one that comes back in under a week without me chasing them. The income approach section is thorough enough that my lender stopped asking for addenda.

James Whitfield

Real Estate Investor

Whitfield Capital Group

Request an

Appraisal Quote.

Three questions and sixty seconds. We'll review the property details and respond with a firm quote within one business day.

Quote within 1 business day — no commitment required

Inspection scheduled within 3 days of engagement

Draft delivered for review before final report

Final signed report in FNMA-compliant PDF format

Your information is used solely to prepare your quote. We do not share data with third parties.

Ready to order your appraisal?

Quotes returned within 1 business day.